It’s Time to File that Tax Return…

The Tax Cuts & Jobs Act of 2017 (TCJA) changed Family Law.

While there was a lot of hype over the TCJA after it was first passed in December of 2017, for most people, the real effect of the tax law changes will be felt with the filing of their 2018 tax return. This is the first of a series of blogs on the new tax law changes affecting the family law world.

Bye, Bye Alimony Deduction!

The TCJA eliminates the alimony deduction. Under prior tax law, alimony payments were included as income to the recipient spouse and deductible to the paying spouse. Often the paying spouse was in a much higher tax bracket than the recipient spouse. This resulted in the paying spouse getting a bigger deduction for alimony payments and enabling the paying spouse to pay more in actual financial support to the recipient spouse. The alimony tax deduction had been around in some form or another since the 1940’s, so the TCJA elimination is significant. Some have argued that the change was necessary because there had been substantial fraud and underreporting. By way of example, less than 47% of those tax returns filed in 2010 that claimed an alimony deduction were matched up with a spouse’s return claiming the alimony as income. Additionally, this change will likely bring in more tax revenue for the federal government.

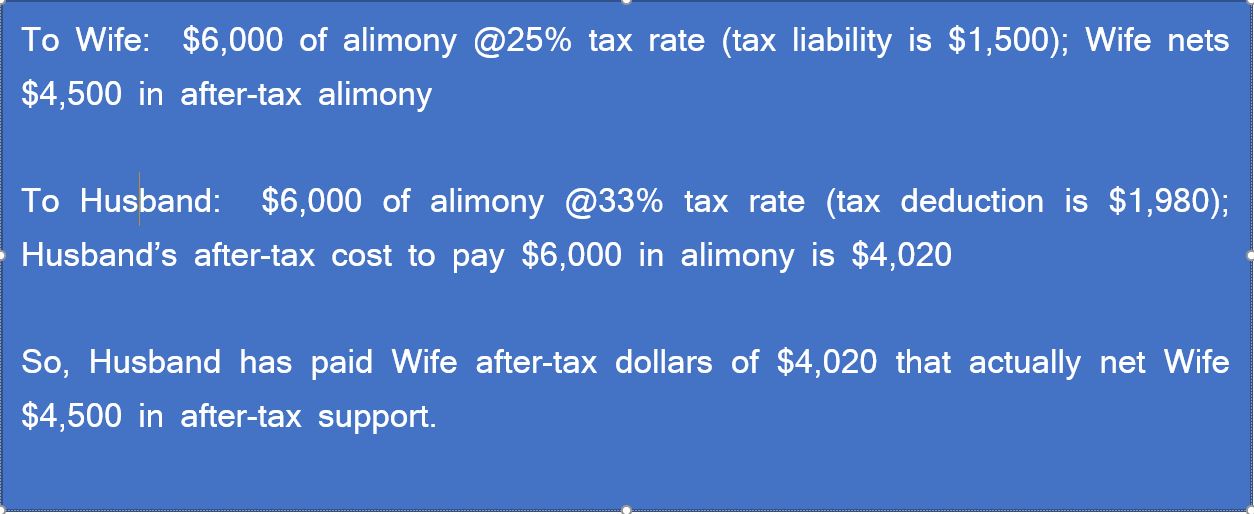

Under the old law, family law attorneys frequently worked closely with accountants to determine the most effective way to maximize the amount of after-tax dollars the family would have to meet their collective needs.

By way of example, assume Wife needs $4,500 per month in order to meet her reasonable needs. Husband earns $267,000 annually, and Wife earns zero. Under the old tax law, if Husband paid Wife $6,000 per month in alimony, Wife’s tax bracket would be 25% and Husband’s would be 33%. The following illustrates what each party would “net” after the tax effect under the old law:

Now consider the same scenario under the TCJA…..

Now consider the same scenario under the TCJA…..

Rather than paying $6,000 in before-tax dollars in alimony to Wife, Husband pays $4,500 in after-tax dollars each month to meet Wife’s needs. Wife has no tax liability on the support payment. She doesn’t have to claim the $4,500 as income because Husband is paying her support with after-tax dollars. Husband’s federal tax rate is 33%. For Husband to net $4,500 in after-tax income, Husband would have to earn over $6,700 in gross income.

In the above example, the tax law change costs Husband over $2,600, as he gets no alimony deduction and instead has to pay Wife with after-tax dollars. There is no difference to Wife, as she still gets $4,500 in net support. However, that assumes that Husband still has the ability to pay Wife $4,500 from his after-tax income. He may not be able to meet his own needs and pay this level of support to Wife.

The only one that benefits in the above example is the federal government. The family has lost out. Assume that Husband had other support obligations to children or to meet his own needs, such that the $2,600 in additional tax liability puts him in a position where he is not able to meet his needs and his support obligations to Wife or the children. There may not be enough after-tax money to pay Wife $4,500. She may end up with less.

Deductible alimony is a thing of the past beginning……January 1, 2019.

The TCJA provides for a permanent repeal of the alimony tax deduction for all support orders or divorce instruments (such as provisions in private contracts like a Separation Agreement) entered on or after January 1, 2019. However, for court orders or divorce instruments entered on or before December 31, 2018, the old law applies and alimony under those particular orders or divorce instruments could be structured as deductible support to the paying spouse and included as income to the receiving spouse.

What if we have a pre-2019 alimony order that gets modified down the road? Does the TCJA apply?

In North Carolina, court-ordered alimony can be modified upon a substantial change in circumstances. This may include a substantial increase or decrease in the recipient spouse’s expenses or condition (i.e., the payee becomes sick or disabled and is unable able to work and contribute to her own needs), or there is a substantial change in the obligor’s ability to provide support (i.e., the obligor is involuntarily unemployed or underemployed, or he becomes disabled or sick). Any alimony order entered before January 1, 2019 that is modified after January 1, 2019 will continue to qualify for the alimony tax deduction. So, for agreements that may be subject to modification, the parties can elect for the alimony to be taxable/deductible or elect for alimony to be non-modifiable under the provisions of the TCJA.

Temporary versus Permanent Orders—which law applies?

In support cases in North Carolina, it is very common for the court to enter an order for temporary spousal support (called Postseparation Support) to provide the dependent spouse with support until the marital property is divided and permanent support (alimony) is determined. With the TCJA, the question is what is the tax effect on alimony paid under an order entered on or after January 1, 2019, that supersedes a postseparation support order that was entered prior to January 1, 2019, in which the spousal support paid is taxable/deductible to the parties under the old law? (That’s a mouth full). Is the alimony under the new order taxable/deductible to the parties? Is the alimony order a modification of the postseparation support obligation? Who knows! The law on its face isn’t clear, and we will have to see how the courts interpret the statute and whether the courts will apply the old law or TCJA in these circumstances interpret this.

Next up……Where is the Dependency Exemption? Is it gone? Or Just Missing?